Creating a budget is one of the most powerful steps you can take toward financial stability and freedom. Whether you’re just starting your career, raising a family, or planning for retirement, understanding where your money comes from and where it goes is essential. In this comprehensive guide, we’ll walk you through the fundamentals of budgeting and help you create a system that works for your unique situation.

Why Budgeting Matters

A budget is simply a plan for your money. It helps you make informed decisions about spending and saving, reduces financial stress, and puts you in control of your financial future. Without a budget, it’s easy to overspend, accumulate debt, or miss opportunities to save for important goals.

Research shows that people who budget regularly are more likely to achieve their financial goals, have less debt, and feel more confident about their financial situation. Even a basic budget can make a significant difference in your financial health.

Step 1: Track Your Income

The first step in creating a budget is understanding exactly how much money you have coming in each month. This includes all sources of income, not just your primary paycheck.

Types of Income to Track:

- Primary employment: Your regular salary or wages (use your net income, or take-home pay, after taxes and deductions)

- Side hustles: Freelance work, gig economy jobs, or part-time employment

- Passive income: Rental income, dividends, interest from savings accounts

- Other sources: Child support, alimony, government benefits, or irregular bonuses

For irregular income, calculate a conservative average based on the past 6-12 months. It’s better to underestimate than overestimate when budgeting.

Step 2: Track Your Expenses

Understanding where your money goes is crucial. Many people are surprised to discover how much they spend on certain categories once they start tracking.

Fixed Expenses

These are expenses that stay relatively the same each month:

- Rent or mortgage payments

- Insurance premiums (health, auto, life, renters/homeowners)

- Loan payments (student loans, car loans)

- Subscription services (streaming, gym memberships, software)

- Phone and internet bills

Variable Expenses

These expenses change from month to month:

- Groceries and dining out

- Utilities (electricity, gas, water)

- Transportation (gas, public transit, rideshares)

- Entertainment and hobbies

- Clothing and personal care

- Medical expenses and medications

- Home maintenance and repairs

How to Track Expenses Effectively

Choose a method that fits your lifestyle:

- Mobile apps: Tools like Mint, YNAB (You Need A Budget), or PocketGuard automatically categorize transactions from linked bank accounts

- Spreadsheets: Create a simple Excel or Google Sheets template to manually log expenses

- Pen and paper: A notebook or budget planner works well for those who prefer analog methods

- Bank statements: Review your statements monthly to identify spending patterns

Track every expense for at least one month to get an accurate picture of your spending habits. You might be surprised by how small purchases add up.

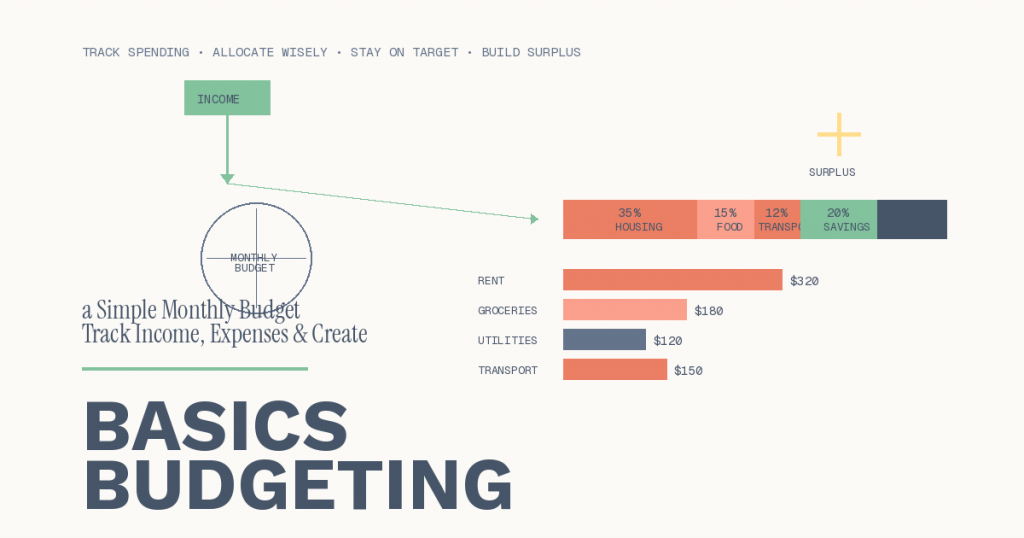

Step 3: Create Your Monthly Budget

Now that you know your income and expenses, it’s time to create a plan. Here’s a simple framework to get started:

The 50/30/20 Budget Rule

This popular guideline divides your after-tax income into three categories:

- 50% for Needs: Essential expenses like housing, utilities, groceries, transportation, insurance, and minimum debt payments

- 30% for Wants: Non-essential spending such as dining out, entertainment, hobbies, and shopping

- 20% for Savings and Debt Repayment: Emergency fund, retirement contributions, extra debt payments, and other savings goals

This is a starting point—adjust the percentages based on your circumstances, location, and financial goals.

Zero-Based Budgeting

With this approach, you allocate every dollar of income to a specific category until you reach zero. This doesn’t mean spending everything; it means assigning purposes to all your money, including savings and investments.

Income – Expenses – Savings = $0

This method ensures you’re intentional with every dollar and can help you identify areas where you’re overspending.

Step 4: Implement and Monitor Your Budget

Creating a budget is just the beginning. The real work comes in sticking to it and making adjustments as needed.

Tips for Success:

- Review weekly: Check your spending against your budget every week to catch overspending early

- Be realistic: Don’t create an overly restrictive budget you can’t maintain

- Build in flexibility: Include a “miscellaneous” category for unexpected small expenses

- Adjust as needed: Your first budget won’t be perfect—refine it based on actual spending

- Use cash envelopes: For categories where you tend to overspend, withdraw cash and only use what’s allocated

- Automate savings: Set up automatic transfers to savings accounts so you “pay yourself first”

Common Budgeting Mistakes to Avoid

Being aware of common pitfalls can help you stay on track:

- Forgetting irregular expenses: Account for annual or semi-annual costs like car registration, property taxes, or holiday spending by setting aside money monthly

- Being too restrictive: Allow yourself some fun money to avoid budget burnout

- Not tracking small purchases: That daily coffee or snack can add up to hundreds of dollars monthly

- Giving up after one bad month: Budgeting is a skill that improves with practice

- Not involving your partner: If you share finances, both people need to be on board

Tools and Resources

Take advantage of technology to make budgeting easier:

- Budgeting apps: Mint, YNAB, EveryDollar, PocketGuard, Goodbudget

- Spreadsheet templates: Free templates from Google Sheets, Microsoft Excel, or personal finance blogs

- Bank tools: Many banks offer built-in budgeting and spending analysis features

- Receipt scanning apps: Expensify, Shoeboxed for tracking business or tax-deductible expenses

Taking the Next Step

A budget is a living document that should evolve with your life circumstances. As you get comfortable with basic budgeting, you can explore more advanced strategies like sinking funds for specific goals, percentage-based budgeting, or expense optimization techniques.

Remember, the goal of budgeting isn’t to restrict your life—it’s to empower you to spend money on what truly matters while building financial security for the future. Start simple, be patient with yourself, and celebrate small wins along the way.

The journey to financial wellness begins with a single step: knowing where your money goes. With the basics of income tracking, expense monitoring, and budget creation under your belt, you’re well-equipped to take control of your financial future.